All Activity

- Past hour

-

Mbjvsdfuftac joined the community

Mbjvsdfuftac joined the community - Today

-

Bcgamer123456789 joined the community

Bcgamer123456789 joined the community -

Cryptoboss Casino — онлайн-казино, где главное — стабильность и комфорт, а не на громкие обещания. Здесь прозрачные механики бонусов и ровная работа без сюрпризов. Если вы предпочитаете чёткие цифры вместо ярких лозунгов, зайдите на Crypto boss casino официальный сайт и оцените всё на практике. В лобби представлены слоты, рулетка, блэкджек и живые столы, причём поиск игр занимает секунды. Платежи в криптовалюте и фиате поддерживаются нативно, выплаты приходят без лишних задержек. Гибкая бонусная система для разных стилей игры Еженедельные ивенты и розыгрыши Ответы быстро и по делу Cryptoboss Casino подойдёт тем, кто ценит порядок и понятные правила

Cryptoboss Casino — онлайн-казино, где главное — стабильность и комфорт, а не на громкие обещания. Здесь прозрачные механики бонусов и ровная работа без сюрпризов. Если вы предпочитаете чёткие цифры вместо ярких лозунгов, зайдите на Crypto boss casino официальный сайт и оцените всё на практике. В лобби представлены слоты, рулетка, блэкджек и живые столы, причём поиск игр занимает секунды. Платежи в криптовалюте и фиате поддерживаются нативно, выплаты приходят без лишних задержек. Гибкая бонусная система для разных стилей игры Еженедельные ивенты и розыгрыши Ответы быстро и по делу Cryptoboss Casino подойдёт тем, кто ценит порядок и понятные правила -

Fbhxihtqgyccvv joined the community

Fbhxihtqgyccvv joined the community -

Zbyfesxufub joined the community

Zbyfesxufub joined the community -

Gumowy23 joined the community

Gumowy23 joined the community -

My web blog :: Betify

- Yesterday

-

AlphaYankeeee joined the community

AlphaYankeeee joined the community -

SAIDULISLAM_BABU changed their profile photo

SAIDULISLAM_BABU changed their profile photo -

BhomaRam joined the community

BhomaRam joined the community -

Error as a result of cancelling a deposit transaction that has not been sent

Error as a result of cancelling a deposit transaction that has not been sent -

dwreck90 joined the community

dwreck90 joined the community - Last week

-

Whatsup people my name is leo i live in mexico 99903140

-

Whatzgood1 joined the community

Whatzgood1 joined the community -

Maxofaxo433 joined the community

Maxofaxo433 joined the community -

Zooma Casino — это не просто место для игры, это настоящая платформа для азартных игр, где любой может найти щедрые предложения и уникальные игры. Zooma casino. Преимущества игры в Zooma Casino: Множество слотов с интересными сюжетами и щедрыми выигрышами. Возможность получать бонусы за активную игру и постоянную активность. Надежные методы пополнения счета и вывода выигрышей, что делает процесс быстрым и безопасным. Доступность мобильной версии, что позволяет играть в любое время. Начните и погрузитесь в мир Zooma Casino прямо сейчас!

-

Cryptoboss Casino — онлайн-казино, которое хорошо вписывается в домашний ритм, когда нужно переключиться после работы. Здесь интерфейс не давит яркими вспышками, а значит, можно просто зайти на Cryptoboss casino официальный и поиграть в комфортном для себя темпе. Игровой каталог даёт возможность подобрать подходящий формат, а всегда можно играть без обязательного участия в промо. Можно играть с выключенным звуком или в наушниках, так что игра легко сочетаетcя с другими делами. Неспешные сессии без гонки за турнирами Операции проходят без лишней нервозности Поддержка, которая не торопит Если вам ближе комфорт, чем гонка, такой стиль будет особенно удобен

-

Visit my web-site ... Jeux du penalty argent

-

4M Dental Implant Center 3918 Longg Beach Blvd #200, Ꮮong Beach, CA 90807, United States 15622422075 rapid aligners

-

Why?

Why?

-

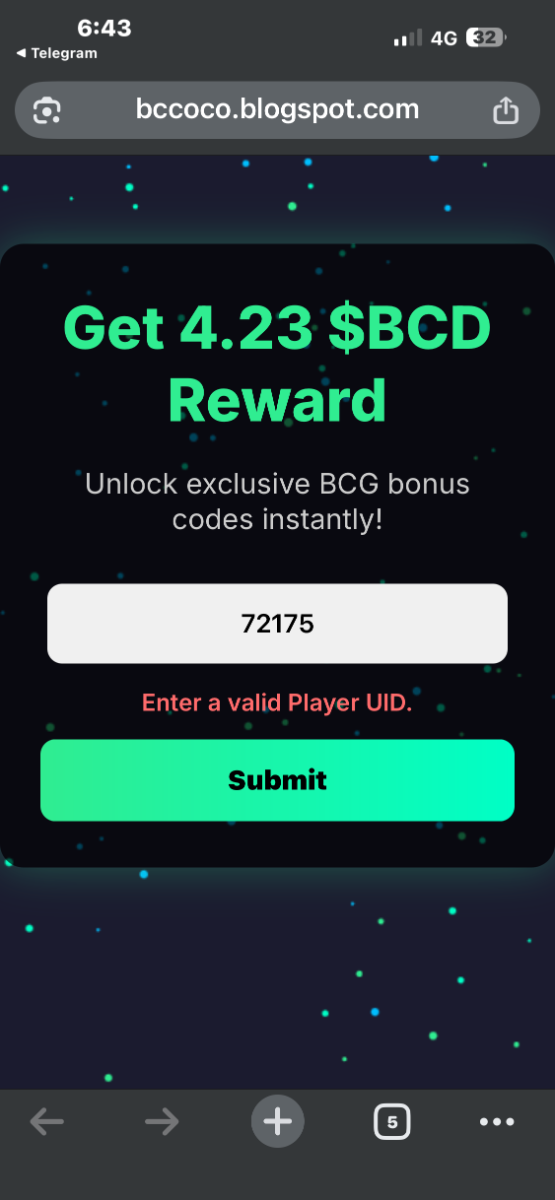

new shitcode Claim Now : 4,23 $BCD Cocco Code valid For All players Lv

Hfrahud replied to Dann_BCGAME's topic in Sports Discussion

Give me bonus code -

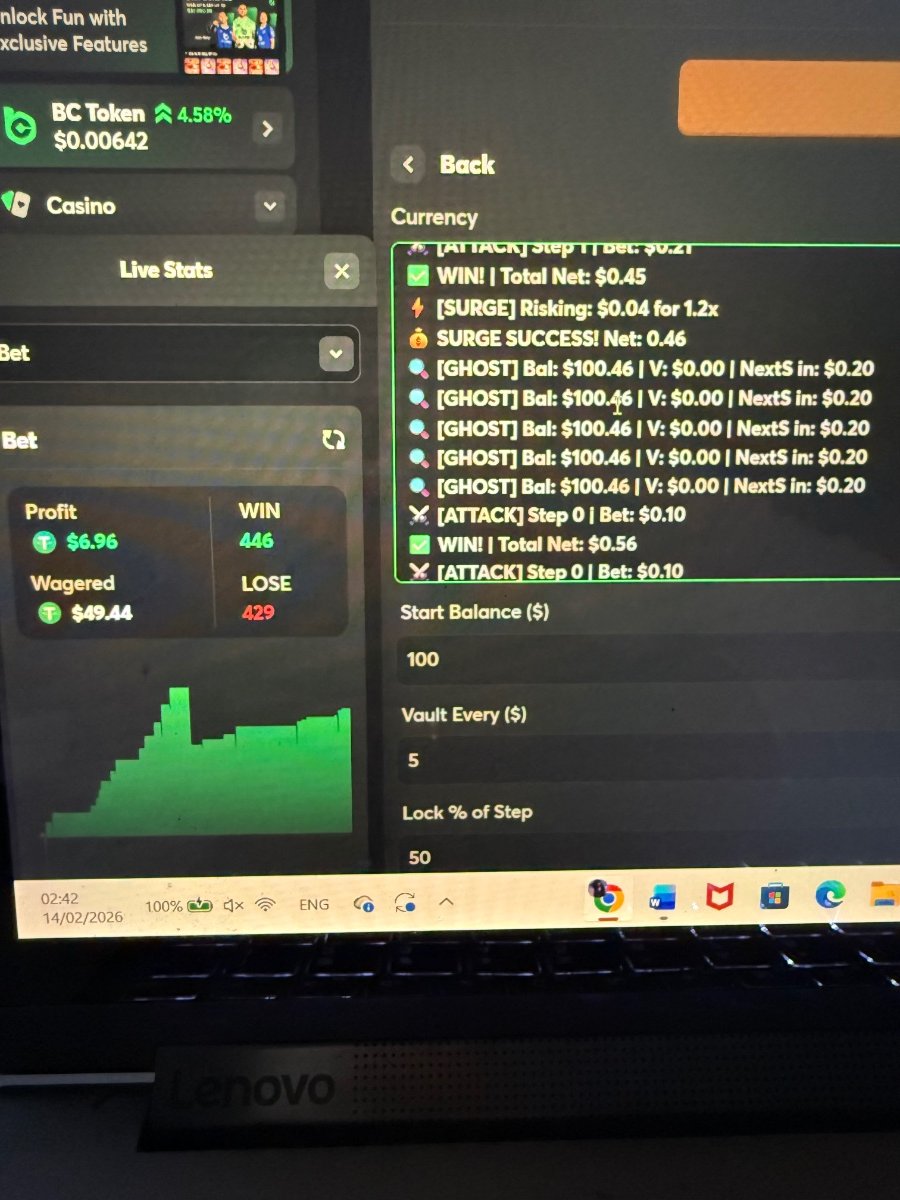

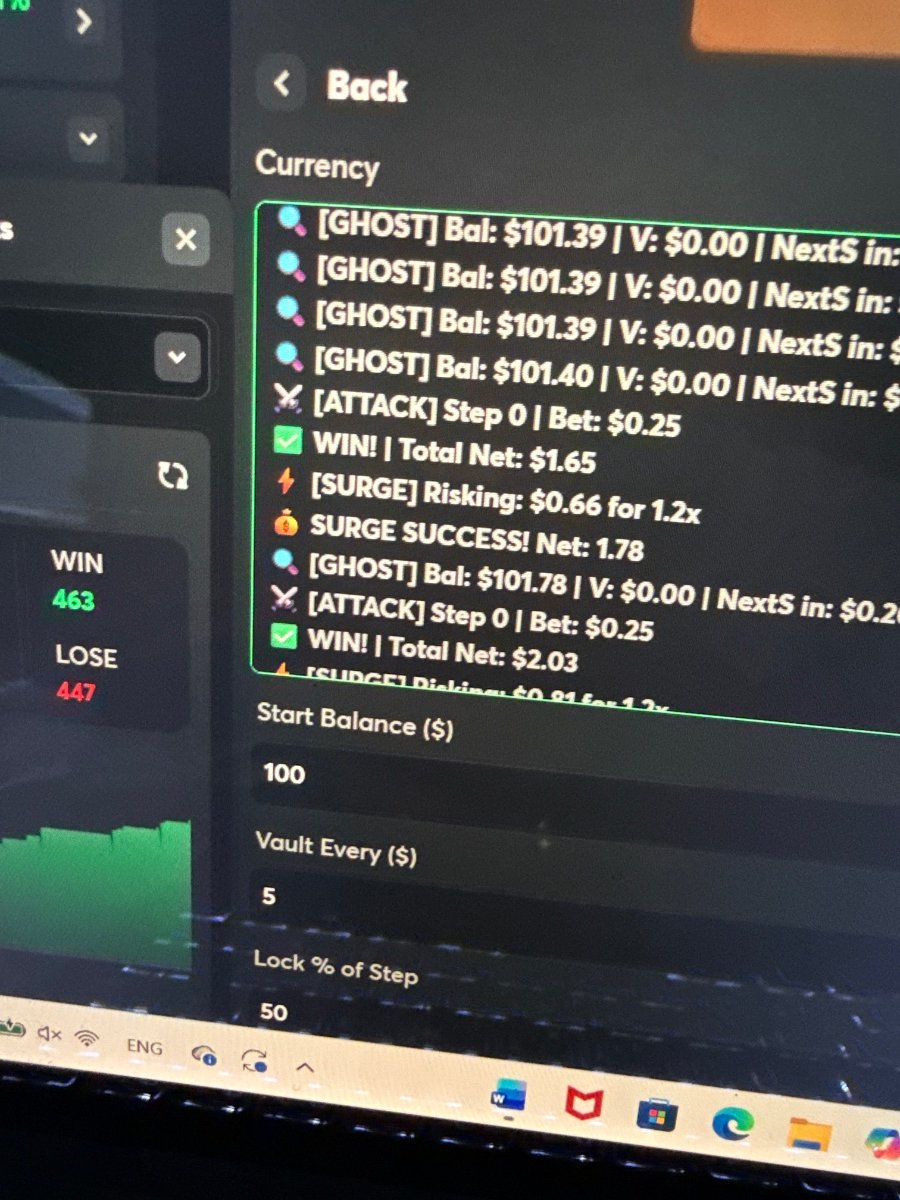

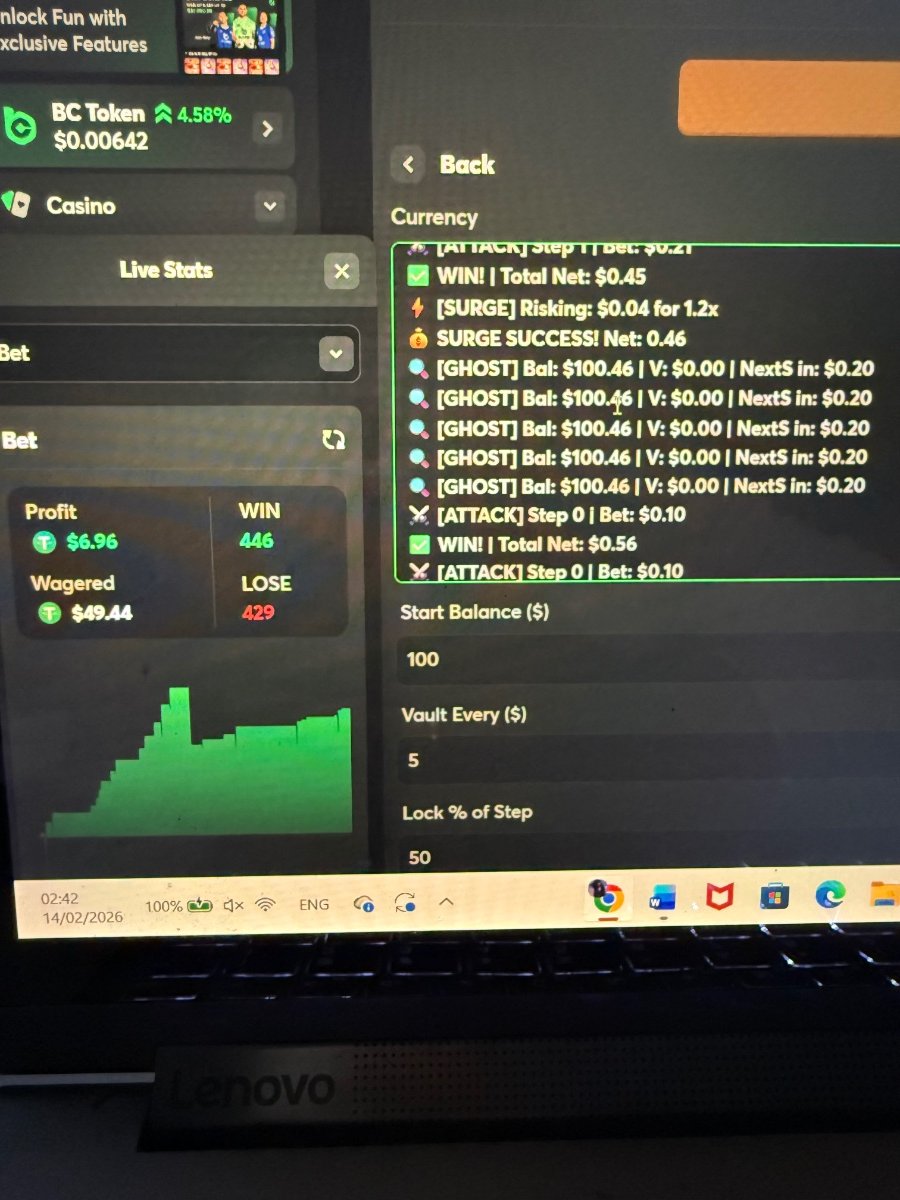

al System Hi everyone, I’ve been refining a new system for a while now, and I wanted to share the results. I call it the Analytical Vault (V11.0). Unlike basic scripts that just follow a fixed pattern, I designed this one with a "brain" that constantly re-calculates its own safety net. It operates across different mental states: GHOST mode for low-risk observation, ATTACK mode for calculated strikes, and a SURGE mode that compounds profits only when the session is going well. The most important part is the Vault mechanism. Every time the system hits a profit milestone, it automatically "locks" a portion of those winnings. It essentially moves the money to a safe area where the script can't touch it, while simultaneously tightening the Stop Loss to protect what’s already been earned. It’s built for players who are tired of winning and then losing it all in one bad streak. It’s about securing the green as you go. I’m looking to share this with a small group of serious, high-tier players. If you understand how a risk-management system like this works and you’re interested, reach out [email protected]

-

Hi everyone, I’ve been refining a new system for a while now, and I wanted to share the results. I call it the Analytical Vault (V11.0). Unlike basic scripts that just follow a fixed pattern, I designed this one with a "brain" that constantly re-calculates its own safety net. It operates across different mental states: GHOST mode for low-risk observation, ATTACK mode for calculated strikes, and a SURGE mode that compounds profits only when the session is going well. The most important part is the Vault mechanism. Every time the system hits a profit milestone, it automatically "locks" a portion of those winnings. It essentially moves the money to a safe area where the script can't touch it, while simultaneously tightening the Stop Loss to protect what’s already been earned. It’s built for players who are tired of winning and then losing it all in one bad streak. It’s about securing the green as you go. I’m looking to share this with a small group of serious, high-tier players. If you understand how a risk-management system like this works and you’re interested, reach out

-

my web blog; Penallty Shoot Out

-

Also visit my web page; Betify casino en ligne

-

Here is my website ... Betify casino

-

T20 World Cup Betting on BC.Game: How to Play Your Cards Right Let’s be honest: T20 cricket is basically the "fast and the furious" of the sporting world. It’s loud, it’s chaotic, and it’s over before you can even finish a decent pizza. But if you’re sitting there watching the T20 World Cup without at least a little bit of skin in the game, you’re missing half the adrenaline. If you’ve been hanging around the Gamblegrounds community for a while, you know we don't just settle for any old bookie. We want fast payouts, crazy markets, and a vibe that doesn't feel like a dusty 1990s betting shop. That’s exactly why BC.Game has become the go-to spot for the "degens" and the pros alike during the World Cup season. Here is the lowdown on how to dominate the T20 World Cup betting scene on BC.Game without losing your shirt (or your sanity). Why BC.Game for the T20 World Cup? Look, there are a million sportsbooks out there, but BC.Game hits differently. If you’re into crypto, it’s a no-brainer. Lightning Fast Moves: In T20, the game flips in one over. You don't have time to wait for a banking page to load. BC.Game’s UI is slick, and if you’re using crypto (BTC, ETH, SOL, whatever), your deposits and withdrawals happen at light speed. The Odds are Actually Decent: A lot of sites "juice" the odds so much during the World Cup that it’s almost impossible to find value. BC.Game stays pretty competitive, especially on the underdog picks. The Chat & The Rains: If the match gets boring (looking at you, rain-delayed games), the community chat is where the real action is. People are tipping, dropping "rains" of free crypto, and complaining about their parlays together. It feels like a pub, but without the sticky floors. The Markets: Beyond the "Match Winner" If you’re only betting on who wins the game, you’re playing it too safe. The beauty of T20 World Cup betting on BC.Game is the sheer variety of ways you can win. Total Sixes: T20 is a power game. Betting over/under on the total number of sixes in a match is a classic move. It makes every swing of the bat feel like a personal win. The Powerplay Hustle: The first six overs are absolute carnage. Betting on the total runs scored in the powerplay is one of the most exciting ways to get an early win before the middle-over lull sets in. Player Performance: Is Virat Kohli going to go beast mode? Is Rashid Khan going to bag three wickets? You can bet on individual player milestones, which is great if you actually follow the players and not just the teams. Pro Tips for the T20 World Cup I’m not going to sit here and give you some "guaranteed win" nonsense—anyone who tells you they have a 100% system is lying to you. But here is how I play it to keep my bankroll from getting rekt. 1. Watch the Toss (But Don’t Overrate It) In some venues, winning the toss and bowling first is a massive advantage because of the dew factor. BC.Game updates their live odds the second the coin hits the ground. Keep your finger on the trigger, but remember: a world-class team can still defend a total if they have the right spinners. 2. Don’t Chase the "Mega-Parlay" We’ve all seen those crazy 12-leg parlays that turn $5 into $5,000. They’re fun, but they’re basically a lottery. If you want to actually build a balance, stick to 2 or 3-leg parlays or "singles" (betting on one match at a time). It’s not as flashy, but your wallet will thank you. 3. Use the BC.Game Rewards BC.Game has some of the best VIP perks in the game. Check your "Recharge" and your "Cashback" settings. During the World Cup, they often run specific promos or boosted odds for the big games (like India vs. Pakistan). If you aren't checking the "Promos" tab every day, you’re literally leaving money on the table. The "In-Play" Vibe The real money (and the real stress) is in Live Betting. T20 is a game of momentum. One wicket can send the odds swinging wildly. If you see a team struggling to find the boundary for a couple of overs, the "Under" on the next 5-over block might be a smart play. BC.Game’s live tracker is decent, but honestly? Have the match on your TV and the BC.Game app on your phone. If you see a bowler starting to lose their line and length, jump on the batting side before the bookie adjusts. A Final Reality Check Betting on the T20 World Cup is meant to make the games more fun, not to pay your mortgage. Set a Limit: Decide how much you’re willing to play with for the whole tournament. If you lose it, you’re done. No chasing losses. Know the Pitch: A match in Barbados plays very differently from a match in New York or Dallas. Do five minutes of homework on the ground stats before you put your money down. If you’re ready to get started, head over to Gamblegrounds.com to check our latest BC.Game reviews and exclusive links. Let’s see if we can catch a few 10x wins this season. Good luck, stay sharp, and let’s hope for plenty of sixes and zero rainouts!

-

Alright, let’s be real for a second. If you’re still waiting three days for a bank wire to clear just so you can play a few rounds of slots, you’re basically living in the Stone Age. The world moved on, and it moved to the blockchain. If you’ve been hanging around the BC.Game forum or scrolling through Gamblegrounds.com, you’ve probably seen the hype. "Crypto Casinos" aren't just a buzzword; they’re a total shift in how we play. But I get it—if you’re new, looking at a Bitcoin wallet address feels like trying to read Matrix code. Don't sweat it. This is your Crypto Casinos 101, and we’re going to use the absolute king of "vibes" games—Plinko—as our training ground. Why Go Crypto? (The Quick Version) Before we drop that first ball, why bother with Bitcoin at all? Instant Gratification: No more "processing" for 48 hours. When you win, that crypto hits your wallet faster than you can say "jackpot." Privacy: Your bank doesn't need to know you enjoy a late-night session. It’s your money; keep it that way. Provably Fair: This is the big one. On sites like BC.Game, you can actually verify that the house didn't cheat you. Every bet is backed by math you can audit yourself. Step 1: Loading the Clip (Your First Deposit) You can't bet if the wallet is empty. To get started, you’ll need some Bitcoin (BTC) or even better for low fees, something like Litecoin (LTC) or Doge. Pro Tip: Don’t overthink it. Grab an exchange account (like Binance or Coinbase), buy a small amount, and hit "Withdraw." The Address: Your casino will give you a long string of random letters and numbers. Copy. Paste. Triple-check. If you send it to the wrong address, that money is gone to the moon, and nobody is coming to get it back. Once those confirmations hit, your balance will light up. Now, the fun starts. Step 2: Plinko — The Ultimate Degen Gateway If you’ve ever watched The Price is Right, you know Plinko. In the crypto world, it’s basically been perfected. It’s simple, it’s visual, and it’s addictive as hell. When you open Plinko on BC.Game, you’ll see a pyramid of pegs. A ball drops from the top, bounces around like a pinball, and lands in a multiplier at the bottom. Here’s the strategy (if you can call it that): Risk Level: You can usually set this to Low, Medium, or High. Low Risk: You won’t lose much, but you won't win much. It’s steady. High Risk: The middle buckets pay almost nothing, but the far-left and far-right buckets? We’re talking 1000x your bet. This is where the legends (and the heart attacks) are made. Rows: You can choose how many rows of pegs to use (usually 8 to 16). More rows = higher potential multipliers, but it’s harder to hit the edges. The "Vibe" Strategy: Most of us degens like to set it to 16 rows, High Risk, and just let a few balls drop while hanging out in the chat. There’s nothing like seeing that ball hug the far right wall and praying it skips one last peg into the big money. Step 3: Navigating the BC.Game Community The best part about crypto gambling isn't just the games; it’s the community. The BC.Game forum is a goldmine. People share their "Big Win" screenshots, complain about a dry spell, and—most importantly—drop Rain and Tips. The Chat: If you’re active and cool, people literally just throw small amounts of crypto at each other. It’s wild. Contests: Always check the forum for Plinko challenges. Sometimes there’s extra moolah for hitting a specific multiplier or even for the most "creative" loss (we’ve all been there). Step 4: The Golden Rules (Don't Get Rekt) Look, I love a good 1000x chase as much as the next guy, but let’s keep it 100. Bankroll Management: Only deposit what you’re okay with losing. Crypto is volatile enough as it is. Don't bet the rent money. The "House Edge" is Real: Even with "Provably Fair" tech, the house still has a tiny edge. It’s entertainment, not a 401k plan. Watch the Fees: If you’re playing small, don't use Bitcoin. The network fees will eat your lunch. Use TRX, LTC, or SOL for those lightning-fast, nearly free moves. Wrapping It Up Crypto casinos are basically the Wild West, but with better graphics and faster payouts. Starting with something like Plinko is the perfect way to get your feet wet without having to learn complex card strategies or sports stats. It’s just you, the pegs, and the gravity. So, head over to Gamblegrounds.com, check out the latest reviews, and maybe pop into the BC.Game forum to say hi. Who knows? Your first Bitcoin bet might just be the one that hits the corner bucket.

Alright, let’s be real for a second. If you’re still waiting three days for a bank wire to clear just so you can play a few rounds of slots, you’re basically living in the Stone Age. The world moved on, and it moved to the blockchain. If you’ve been hanging around the BC.Game forum or scrolling through Gamblegrounds.com, you’ve probably seen the hype. "Crypto Casinos" aren't just a buzzword; they’re a total shift in how we play. But I get it—if you’re new, looking at a Bitcoin wallet address feels like trying to read Matrix code. Don't sweat it. This is your Crypto Casinos 101, and we’re going to use the absolute king of "vibes" games—Plinko—as our training ground. Why Go Crypto? (The Quick Version) Before we drop that first ball, why bother with Bitcoin at all? Instant Gratification: No more "processing" for 48 hours. When you win, that crypto hits your wallet faster than you can say "jackpot." Privacy: Your bank doesn't need to know you enjoy a late-night session. It’s your money; keep it that way. Provably Fair: This is the big one. On sites like BC.Game, you can actually verify that the house didn't cheat you. Every bet is backed by math you can audit yourself. Step 1: Loading the Clip (Your First Deposit) You can't bet if the wallet is empty. To get started, you’ll need some Bitcoin (BTC) or even better for low fees, something like Litecoin (LTC) or Doge. Pro Tip: Don’t overthink it. Grab an exchange account (like Binance or Coinbase), buy a small amount, and hit "Withdraw." The Address: Your casino will give you a long string of random letters and numbers. Copy. Paste. Triple-check. If you send it to the wrong address, that money is gone to the moon, and nobody is coming to get it back. Once those confirmations hit, your balance will light up. Now, the fun starts. Step 2: Plinko — The Ultimate Degen Gateway If you’ve ever watched The Price is Right, you know Plinko. In the crypto world, it’s basically been perfected. It’s simple, it’s visual, and it’s addictive as hell. When you open Plinko on BC.Game, you’ll see a pyramid of pegs. A ball drops from the top, bounces around like a pinball, and lands in a multiplier at the bottom. Here’s the strategy (if you can call it that): Risk Level: You can usually set this to Low, Medium, or High. Low Risk: You won’t lose much, but you won't win much. It’s steady. High Risk: The middle buckets pay almost nothing, but the far-left and far-right buckets? We’re talking 1000x your bet. This is where the legends (and the heart attacks) are made. Rows: You can choose how many rows of pegs to use (usually 8 to 16). More rows = higher potential multipliers, but it’s harder to hit the edges. The "Vibe" Strategy: Most of us degens like to set it to 16 rows, High Risk, and just let a few balls drop while hanging out in the chat. There’s nothing like seeing that ball hug the far right wall and praying it skips one last peg into the big money. Step 3: Navigating the BC.Game Community The best part about crypto gambling isn't just the games; it’s the community. The BC.Game forum is a goldmine. People share their "Big Win" screenshots, complain about a dry spell, and—most importantly—drop Rain and Tips. The Chat: If you’re active and cool, people literally just throw small amounts of crypto at each other. It’s wild. Contests: Always check the forum for Plinko challenges. Sometimes there’s extra moolah for hitting a specific multiplier or even for the most "creative" loss (we’ve all been there). Step 4: The Golden Rules (Don't Get Rekt) Look, I love a good 1000x chase as much as the next guy, but let’s keep it 100. Bankroll Management: Only deposit what you’re okay with losing. Crypto is volatile enough as it is. Don't bet the rent money. The "House Edge" is Real: Even with "Provably Fair" tech, the house still has a tiny edge. It’s entertainment, not a 401k plan. Watch the Fees: If you’re playing small, don't use Bitcoin. The network fees will eat your lunch. Use TRX, LTC, or SOL for those lightning-fast, nearly free moves. Wrapping It Up Crypto casinos are basically the Wild West, but with better graphics and faster payouts. Starting with something like Plinko is the perfect way to get your feet wet without having to learn complex card strategies or sports stats. It’s just you, the pegs, and the gravity. So, head over to Gamblegrounds.com, check out the latest reviews, and maybe pop into the BC.Game forum to say hi. Who knows? Your first Bitcoin bet might just be the one that hits the corner bucket. -

thetexaslawdog01 changed their profile photo

thetexaslawdog01 changed their profile photo -

Accidents have a way of changing everything in seconds. One moment you’re driving home, and the next you’re dealing with pain, paperwork, insurance calls, and a lot of unanswered questions. That’s where The Texas Law Dog steps in clear headed, battle ready, and focused on protecting people who never asked to be in this situation as a Texas Personal Injury Lawyer, the goal is simple: take the legal stress off your plate so you can focus on healing. No scare tactics. No fancy legal talk. Just honest guidance and aggressive representation when someone else’s mistake causes real harm. Car accidents can leave you injured, frustrated, and overwhelmed. Insurance companies often move fast not to help, but to protect themselves. As experienced Car Wreck Lawyers, The Texas Law Dog knows how to slow things down, dig into the details, and fight for compensation that actually reflects what you’ve been through. Truck accidents are even more complex. Bigger vehicles mean bigger damage, more serious injuries, and companies that fight hard to avoid responsibility. Skilled Truck Wreck Lawyers understand federal regulations, driver logs, and corporate defenses and aren’t afraid to go nose-to-nose with them. The Texas Law Dog believes injured Texans deserve respect, straight answers, and a lawyer who shows up ready to work. When life throws a hard hit your way, you shouldn’t have to face it alone. Consider this your legal backup loyal, relentless, and always on your side. https://thetexaslawdog.com/practice-areas/ https://www.facebook.com/thetexaslawdog/ https://www.instagram.com/texaslawdogs/ https://www.youtube.com/@TheTexasLawDog https://x.com/TexasLawDogs https://www.linkedin.com/company/aulsbrook-law-firm/

- Earlier

-

Earn 4,23 $BCD Cocco Code valid For All players Lv

Awal12 replied to BCGAME_Dann's topic in Sports Discussion

Cocco Tolong beritahu saya hadiah itu.. jika itu serius -

很高兴认识大家。我是新来的,想借此机会自我介绍一下。我浏览论坛已经有一段时间了,非常喜欢这里的讨论和社区氛围,所以决定正式加入进来。 简单介绍一下我自己:我对在线工具、数字产品以及科技如何让内容创作更轻松便捷很感兴趣。闲暇时,我喜欢探索新平台、测试人工智能工具,并学习人们如何创造性地使用它们——尤其是在视频和社交媒体内容方面。 最近,我花了一些时间开发一个名为“文本转视频工具”的小项目。这是一个基于人工智能的工具,可以将文本转换成短视频。我最初开发这个项目主要是出于对人工智能和内容工作流程的个人兴趣,到目前为止,这对我来说是一次非常宝贵的学习经历。我一直很想了解其他人是如何进行内容创作或自动化的。 我期待着向大家学习,参与讨论,并在力所能及的范围内做出贡献。如果您有任何给新手的建议,或者有什么有趣的帖子值得我关注,请随时告诉我。 谢谢邀请,很高兴成为社区的一份子! Textideo is a next-generation AI video creation platform built for content creators and influencers. Simply turn text into high-quality videos designed for YouTube, TikTok, and Instagram. Powered by the advanced Veo 3.1 model, Textideo delivers cinematic 1080p visuals with fine control over composition, lighting, and pacing. With support for multi-shot sequences and consistent visual styles, you can easily create cohesive, story-driven content that keeps viewers engaged. Built-in AI effects, GIF generation, and video enhancement tools help your videos stand out. With Textideo, transforming ideas into compelling visuals has never been easier.

-

NBA | Boston Celtics vs Golden State Warriors - Jun 11 | 01:00 UTC

Chibu6 replied to Mat's topic in Sports Discussion

-

Earn 4,23 $BCD Cocco Code valid For All players Lv

Chibu6 replied to BCGAME_Dann's topic in Sports Discussion

-

Sir please mera deposit nahi hua hai fast aad I'd PR add kar

-

Claim Now : 4,23 $BCD Cocco Code valid For All players Lv

MuratRumpel23 replied to Dann_BCGAME's topic in Sports Discussion

Code? -

Claim Now : 4,23 $BCD Cocco Code valid For All players Lv

fgonser1 replied to Dann_BCGAME's topic in Sports Discussion

.